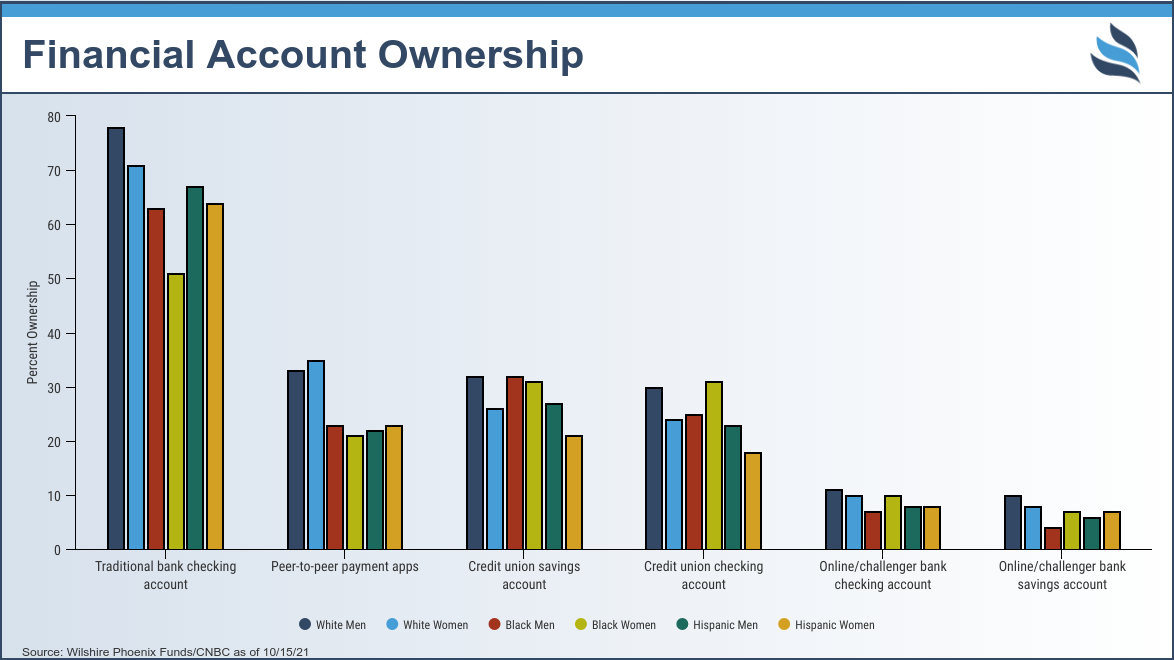

- Opening a bank account may be something that most take for granted – while 70% of people in the United States own a traditional bank account, there is stark contrast amongst race and gender for account ownership.

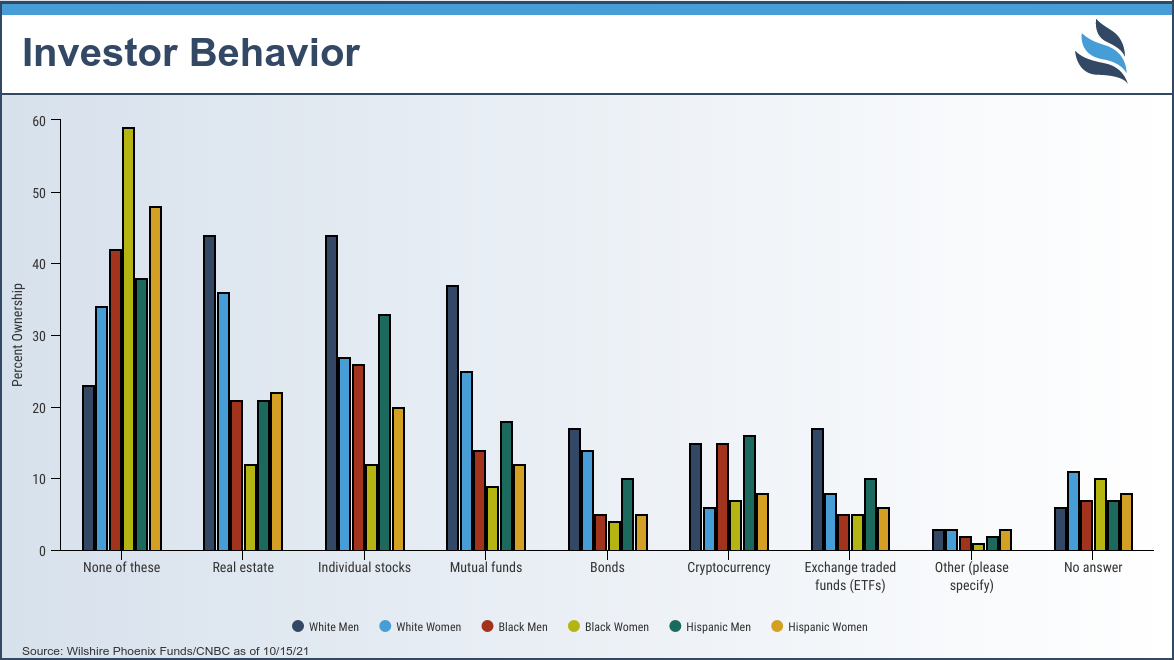

- Only 50% of households in the U.S. own equities directly, with women citing lack of funds and education as reasons for not investing.

- Socio-economic factors such as education and wealth inequality are gating factors to access traditional institutions.

Imagine living without access to a checking or savings account or being unable to use a credit card. That is the reality for 7 million households in the United States (1). It is not that people who are unbanked do not want to have a traditional bank account, but that often they do not have the option. In addition to the unbanked, 20% of the U.S. population is underbanked. While the underbanked may have some type of account, they still rely on alternative means of financing like money orders and payday loans. Socio-economic factors such as education, lack of access to the internet, wealth inequality, and racism gate access to traditional financial institutions and services.

Traditional Banks and Neobanks

People and communities of color have been historically underserved by traditional banking institutions. There are more banks opened in majority White areas – while banks in Black and Latinx communities close at a higher rate during uncertain economic times, creating ‘banking deserts’ (2). High fees and opening minimums are cited as being additional reasons amongst the unbanked for inability to open accounts (1). The unbanked and underbanked are left to use means such as prepaid debit cards, money orders, check cashing or payday loans, which often have high-cost fees, thus perpetuating a vicious cycle of economic inequality (3).

While 70% of adults in the U.S. own a traditional bank account, there is stark contrast amongst race and gender when it comes to bank account ownership. Over 75% of White men report having a traditional bank account, while only 63% of Black men and 67% of Hispanic men do. The number of women who hold accounts shows both a gender disparity and a more drastic racial divide. 71% of White women have a bank account, while only 51% of Black women and 63% of Hispanic women do (4).

“Venmo me”, “send it to me on PayPal” have become everyday phrases in recent years. PayPal, Square, and similar peer-to-peer money transfer apps have become an increasingly popular way to pay for goods and services or conduct peer-to-peer (P2P) money transfers. Indeed, these online services and apps, also known as neobanks, are innovating and helping to serve the unbanked and underbanked. However, neobanks are unable to provide the critical products and services that traditional banks offer in their normal course of business. These fintech companies need to ‘partner’ with ‘real’ financial institutions in order to operate, thus offering no physical presence – which is needed for many.

Access to Investment Products

Only 50% of people in the U.S. own equities directly, and similarly only about 50% own mutual funds or exchange-traded funds (5). 40% of women do not own any investments, with a much higher rate of women of color not owning investments, 59% of Black women and 48% of Hispanic women (4). The primary reasons for women not investing are cited as lack of funds, not knowing how to invest, and perceived risk. Poor financial education being one of the factors stopping women from investing continues the cycle of not seeing investments as a possible way to better their or their families’ futures.

Other Influencing Matters

Education and access to the internet need to be highlighted when discussing people who are unbanked (1). Financial guidance and investment websites, social media, news websites, and discussions with friends and family are the largest means of researching investment ideas across race and gender. Direct discussions with brokers or financial advisors are more common amongst White men and women than Black and Hispanic men and women. Internet access today is critical, not only does it allow people to do their own research and trading, but it is also a means for people to use their money through neobanks in a society that is increasingly favoring digital/paperless payments. 57% of people in the U.S. who make less than $30,000 a year have home broadband, compared to 87% who make $50-75,000 a year (6).

When looking at the statistics by education, 81% of those with a college education have a bank account, while 65% of those who reported as having a high school (or less) or some college education have a bank account. The rates of college-educated individuals who have invested in real estate, stocks, mutual funds, bonds, or ETFs are almost double those who have a lower level of education (5). The financial markets, including the stock market, over the long term, have generated returns for people to buy homes, to pay for their kids’ educations, to start businesses, to prepare for retirement, and in short to live the American dream. Poor financial education hides this opportunity from many even in today’s digital world.

Conclusion

People may not want a bank account for various reasons but regardless, everyone deserves fair and equal access to financial services which can give them the ability to create a better future for themselves and their families. While mobile and online platforms that provide banking services are an option for the unbanked, the commercial and profit-driven priorities of these companies often target areas where the most money can be made, rather than towards helping the people that need it the most. The U.S. government is charged with protecting its citizens- while it does not dictate how one should use, spend, or invest his or her money, it should make sure that opportunities are available to everyone. With the private sector falling short in lifting the unbanked and underbanked, the U.S. government should seek ways to help address this failing through incentives, policies, or law-making; not to intervene but to re-examine and amend the framework for today’s markets. In free markets, people come together in an exchange of ideas, capital, and labor for the benefit of all. The government and private sector must work together to make sure the most vulnerable are not shut out of the opportunities of the free markets.

Sources

1. https://www.economicinclusion.gov/downloads/2019_FDIC_Unbanked_HH_Survey_Report.pdf

2. https://www.newamerica.org/family-centered-social-policy/reports/racialized-costs-banking/the-racialized-costs-of-banking

3. https://libertystreeteconomics.newyorkfed.org/2021/06/banking-the-unbanked-the-past-and-future-of-the-free-checking-account/

4. https://cnb.cx/3ku3YQz

5.https://www.federalreserve.gov/econres/scf/dataviz/scf/chart/#series:Stock_Holdings;demographic:all;population:1;units:have

6. https://www.pewresearch.org/internet/fact-sheet/internet-broadband/?menuItem=2ab2b0be-6364-4d3a-8db7-ae134dbc05cd

THE INFORMATION CONTAINED HEREIN REPRESENTS THE AUTHOR’S SUBJECTIVE BELIEF AND IS NOT AND SHOULD NOT BE CONSTRUED AS INVESTMENT ADVICE. THE INFORMATION AND OPINIONS PROVIDED HEREIN SHOULD NOT BE TAKEN AS SPECIFIC ADVICE ON THE MERITS OF ANY INVESTMENT DECISION. INVESTORS SHOULD MAKE THEIR OWN DECISIONS AND SHOULD NOT RELY ON THE INFORMATION CONTAINED HEREIN. NEITHER THE AUTHOR NOR ANY OF HIS AFFILIATES ACCEPT ANY LIABILITY WHATSOEVER FOR ANY DIRECT OR CONSEQUENTIAL LOSS HOWSOEVER ARISING, DIRECTLY OR INDIRECTLY, FROM ANY USE OF THE INFORMATION CONTAINED HEREIN. THIS INFORMATION IS BASED ON DATA FOUND IN INDEPENDENT INDUSTRY PUBLICATIONS. ALTHOUGH WE BELIEVE THE DATA TO BE RELIABLE, WE HAVE NOT SOUGHT, NOR HAVE WE RECEIVED, PERMISSION FROM ANY THIRD-PARTY TO INCLUDE THEIR INFORMATION IN THIS ARTICLE. MANY OF THE STATEMENTS CONTAINED HEREIN REFLECT OUR SUBJECTIVE BELIEF.